South Africa has one of the most dynamic fintech ecosystems on the African continent. Cape Town and Johannesburg attract investment, talent and regulatory attention. But travel two hours north from Johannesburg, into the smallholder farming communities of Limpopo, and a different reality emerges: no bank branch, no credit history and no documentation that fits a standard onboarding form.

That gap is where the most interesting fintech South Africa story is being written. Not in the venture-funded app studios, but in the alliances between mobile operators, rural cooperatives, agritech platforms and public agencies building financial infrastructure from the ground up.

| 18M+ SASSA grant recipients Many without bank access | 1,200% Deepfake fraud surge Year-on-year, SA fintechs | 60%+ Inclusive initiatives Involve 3+ sectors (FINASA) |

An Ecosystem That No Longer Operates in Silos

For most of the last decade, banks and fintechs in South Africa ran parallel tracks. Banks had the licences and the balance sheets; fintechs had the speed and the UX. They competed more than they collaborated, and neither was particularly effective at reaching the 11 million South Africans still classified as financially excluded.

That model is breaking down, in a good way.

The pattern gaining ground today brings together mobile operators, agritech platforms, rural cooperatives, public agencies and specialised lenders into a shared services layer. The logic is simple: no single actor has all the data, all the trust and all the distribution needed to serve a rural community. But together, they do.

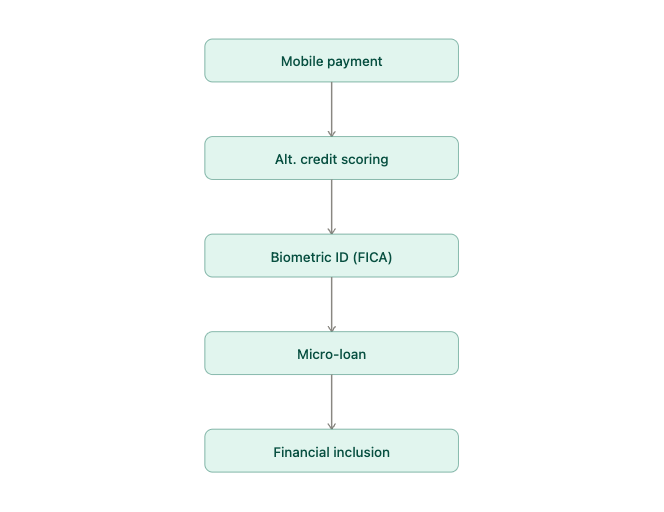

Key insight: Agricultural microcredit built on mobile payment history is the clearest expression of this shift. A farmer in Limpopo who has never held a bank account can unknowingly build a credit profile through prepaid top-ups, utility payments and purchases via MTN mobile money. That behaviour, processed by alternative scoring models, lets fintechs assess risk and offer loans calibrated to harvest cycles, without a single visit to a branch.

According to the Fintech Association of South Africa (FINASA), more than 60% of active financial inclusion initiatives in the country involve at least three distinct sectors. Collaboration is not a trend here; it is a structural condition of the market.

How mobile data becomes credit access: the rural inclusion pipeline

Each step connects an operator, a fintech and a regulator. None of them works alone.

Public-Private Alliances: Where Scale Actually Comes From

The South African state is not a passive observer in this ecosystem. SASSA distributes permanent social grants to more than 18 million beneficiaries, not including the separate SRD grant, many of them in areas where the nearest ATM is a 40-minute taxi ride away. Digitising those payments has not just reduced friction; it has created an entirely new entry point for financial services.

PPP programmes linking SASSA with mobile operators and fintechs are producing something structural: a financial services Africa infrastructure that works bottom-up. The grant recipient receives their payment into a digital wallet, pays a utility bill, tops up their phone and, without knowing it, begins generating a financial behaviour record. Over time, that record translates into credit eligibility.

How the Multi-Sector Model Compares to Traditional Banking

| Dimension | Traditional Bank | Multi-Sector Fintech Model |

|---|---|---|

| Onboarding | In-person, document-heavy | Remote, mobile-first, biometric |

| Credit scoring | Formal history required | Alternative data (mobile, agri, energy) |

| Distribution | Branch network | Mobile operator + cooperative + NGO |

| Identity verification | Paper ID at branch | Digital identity (FICA-compliant) |

| Reach in rural areas | Limited | Structural by design |

| Regulatory framework | Banking Act | FICA + POPIA + SARB payment licences |

Vodacom and MTN, the country’s two largest operators, already run mobile money South Africa platforms with tens of millions of active users. The integration of those platforms with verified digital identity is the logical next step: without securely identifying the user, there is no credit, no insurance and no regulated financial product.

Biometric Identity: The Layer Everything Else Depends On

The biggest barrier to rural financial inclusion in South Africa is not capital or connectivity.

It is identity.

Without a verified document, without a face the system can authenticate, a person remains excluded from any regulated financial product, regardless of how much mobile data they generate. You can have perfect payment behaviour and still be invisible to a lender.

Regulatory context: FICA and Smart ID. The FICA (Financial Intelligence Centre Act) already permits non-face-to-face onboarding, provided that customer identity is verifiably confirmed. Since September 2025, the revised Guidance Notice 7A has tightened the requirements: institutions must implement risk-based CDD, maintain records for at least five years and apply enhanced due diligence for higher-risk customers.

South Africa is also rolling out its national Smart ID system, integrated biometrics for accessing both public and private services, expected to reach full deployment between 2025 and 2029. When a citizen can legally verify their digital identity from a low-end smartphone, bank onboarding and credit access can be completed in under two minutes, remotely, with zero branch involvement.

That makes facial biometrics with liveness detection a functional requirement, not a UX upgrade. Fintechs targeting the inclusive segment need digital identity South Africa solutions that are FICA-compliant and accessible on devices that cost under $100.

Platforms like Facephi’s biometric onboarding solutions combine document capture, facial recognition and liveness detection in a single flow, optimised for low latency on limited mobile networks, precisely the constraint that rural South African deployment demands.

Agritech and Distributed Energy: The Sectors Extending the Map

Rural financial inclusion in South Africa is not running through banks. It is running through solar panels and satellite imagery.

Agritech companies such as Aerobotics and Khula Enterprise Finance are building agricultural risk profiles from satellite crop data, historical yield records and prior payment behaviour. That sector-specific scoring feeds into microfinance South Africa platforms to offer seasonal financing to smallholder farmers who would otherwise be turned away by any standard credit product.

In the energy sector, the pay-as-you-go model applied to distributed solar has proven to be a remarkably effective bancarisation channel. Customers pay weekly instalments via mobile, build a credit history, and in many cases that initial relationship with an energy fintech becomes their entry point to savings products, insurance and eventually formal credit.

Data point: Across emerging markets, economies where energy, telecoms and finance sectors converge see a measurable acceleration in financial inclusion rates among previously excluded populations. South Africa is one of the clearest examples of that convergence in action.

Inclusive Fintech: From Concept to Replicable Infrastructure

The concept of inclusive fintech has been discussed for years. In South Africa, it is finally finding the conditions to scale.

Mature mobile infrastructure. A regulatory framework in continuous evolution: FICA, POPIA, SARB’s digital payment licensing regime. And genuine, unmet demand from communities that have been waiting for financial products that actually fit their lives.

What distinguishes the programmes that work is not the technology. It is the architecture of the alliances. A joint government, mobile operator and fintech programme that shares data, infrastructure and risk has a far greater capacity to reach remote communities than any single actor working alone.

Anatomy of a Successful Financial Inclusion Alliance

| Actor | What They Bring | What They Get |

|---|---|---|

| Government (SASSA) | Distribution to 18M+ grant recipients | Digital payment infrastructure, AML compliance |

| Mobile operator (MTN, Vodacom) | Network, wallet, user trust | New revenue streams, data assets |

| Fintech (Rain Payments, etc.) | Credit scoring, product design | Customer base, regulatory cover |

| Agritech / Energy | Sector data, rural relationships | Embedded financial products |

| Identity provider (e.g. Facephi) | FICA-compliant verification | Strategic positioning in inclusion stack |

Verified digital identity is the glue that keeps this ecosystem functioning. Without it, every alliance has to independently solve the problem of KYC verification authenticating the user, and they will do it inconsistently, expensively and at the cost of user experience.

South Africa’s POPIA adds a further layer of requirement: biometric and financial data must meet standards equivalent to European data protection law. This favours solutions that identity verification platform embed privacy by design and comply with international frameworks such as eIDAS and ISO 27001.

The South African Reserve Bank (SARB) is driving regulatory modernisation on multiple fronts simultaneously: new payment licences, tighter AML oversight, enhanced consumer protection. In that environment, fintechs that operate with auditable, verified identity infrastructure do not just reduce compliance risk. They build the kind of institutional trust that opens the door to larger partnerships, better pricing and sustained growth.

Frequently Asked Questions

Mobile money allows users to make payments, transfers and other transactions via mobile phone, without needing a bank account. In South Africa, MTN and Vodacom run the largest platforms, with tens of millions of active users. Many rural residents use mobile money as their primary, and only, financial tool.

SASSA distributes permanent social grants to more than 18 million South Africans (not including the separate SRD grant). Digitising those payments through mobile wallets has created a de facto entry point for financial services: once a beneficiary is in the digital payment system, the pathway to savings, credit and insurance becomes structurally much shorter.

Without verified identity, access to regulated financial products is legally blocked. Facial biometrics with liveness detection allows the onboarding process to be completed remotely and securely under FICA. In rural communities where the nearest bank branch may be hours away, that is not a convenience feature, it is the entire access model.

Agritech and distributed solar energy are the two most active vectors. Both generate recurring mobile payment behaviour that feeds alternative credit scoring models, enabling microfinance platforms to offer products adapted to the actual economic cycles of rural communities, rather than forcing those communities to fit into products designed for urban salaried workers.

FICA requires institutions to verify customer identity, apply risk-based due diligence and maintain records for a minimum of five years. The revised Guidance Notice 7A (September 2025) permits fully remote onboarding as long as identity verification meets defined standards. For fintechs, this means biometric verification is not optional, it is the legal gateway to operating a compliant digital onboarding flow in South Africa.